On August 16, while responding to queries by the media on the ongoing issue of soaring fuel prices, Union Finance Minister Nirmala Sitharaman claimed, “UPA government had reduced fuel prices by issuing oil bonds of ₹1.44 lakh crore. I can’t go by the trickery that was played by the previous UPA government. Due to oil bonds, the burden has come to our government. We are bleeding to pay the oil bonds of ₹1.44 lakh crore of the UPA government.”

She added, “We’ll still have to pay interest of ₹37,000 crore by 2026. Despite interest payments, a principal outstanding of over ₹1.30 lakh crore is still pending. If I didn’t have the burden of oil bonds, I would have been in a position to reduce excise duty on fuel.”

The following media outlets carried Sitharaman’s statement on face value — Livemint, Free Press Journal, Zee News, News18, Zee Business, and Latestly. Most of these articles are based on the reports carried by ANI and PTI.

BJP had made the same claim in 2018.

What the economist PM Manmohan Singh said & did on petroleum prices? He said that money does not grow on trees & left unpaid bills of oil bonds worth Rs. 1.3 lakh crore. Modi govt paid off the pending bills with interest because ‘we should not burden our children’. #NationFirst pic.twitter.com/Z8zTV1kG1i

— BJP (@BJP4India) September 10, 2018

FACT-CHECK

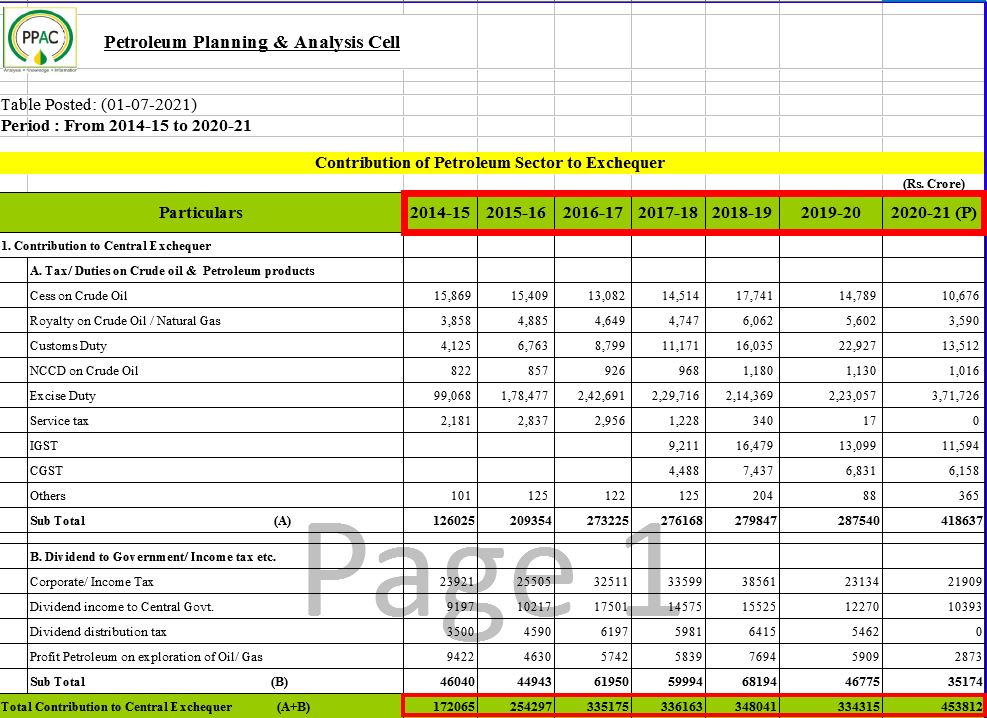

While Nirmala Sitharaman blamed the interest paid on oil bonds issued during the UPA government for her inability to reduce excise duty on fuel, the math doesn’t add up. The earnings from the petroleum sector to the central government in 2021-22 (₹4.5 lakh crores) is significantly greater than the sum of the principal amount (₹1.44 lakh crore of oil bonds issued) and total interest (almost as much as the principle) on the principal amount. Since coming to power, the BJP government has paid back ₹3,500 crores of the principal amount and approximately ₹10,000 crores annual as interest as of August 22, 2021.

Before we get into why oil bonds were issued, what are oil bonds, assessment of their impact on current fuel, it is important to understand the impact of inflation of fuel prices on the economy.

IMPACT OF INFLATED FUEL PRICES

India’s demand for fuel is largely met via import. Thus, the impact of the increase in global fuel prices is on India’s trade deficit. However, an increase in domestic fuel prices has both seen and unseen effects because it impacts retail prices of all other commodities manufactured using crude. For instance, vegetable prices shoot up because of the increased cost of transportation.

In July, Alt News reported that approximately 33% of fuel’s retail price per litre goes to the central government as excise duty. In June, ICRA Limited, professional investment information and credit rating agency, said that the union government has room to cut the cess it levies on petrol and diesel by ₹4.5 per litre without losing revenues, to ease inflationary pressure.

WHY WERE OIL BONDS ISSUED?

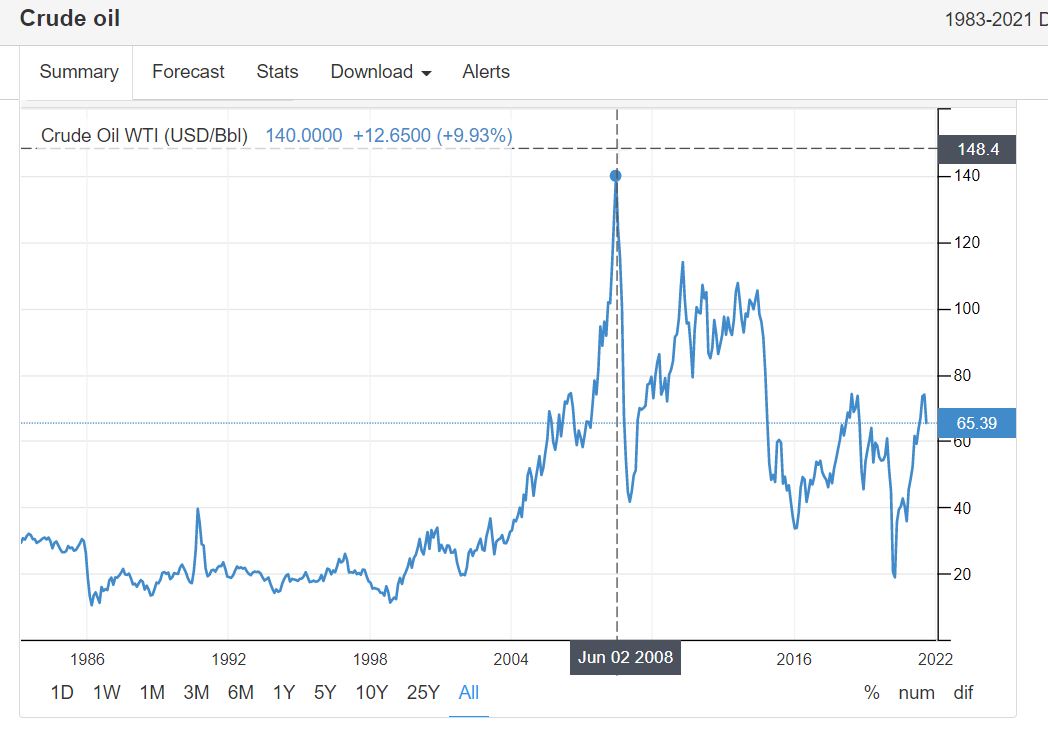

Global crude oil prices prior to 2014 (during the UPA government) were significantly higher as compared to prices under the BJP government. Yet, the fuel prices under UPA were cheaper than current prices.

How did UPA achieve that? Finshots, a finance newsletter platform co-founded by IIM Ahmedabad alumni Bhabu Harish Gurram, explains, “Back in 2005, the UPA government had a massive problem on its hands. They were trying to fix the price of oil in a bid to make fuel more accessible to the general public. They subsidized the price of oil by setting aside a portion of their budget [known as under-recoveries]. And to their credit [in form of oil bonds], they continued to do this until they realized they could do this no more.”

It is pertinent to note that in 2006 the Committee on Pricing and Taxation of Petroleum Products stated, “The practice of issuing oil bonds is strictly inadvisable as it does not resolve the problem; it only postpones the resolution while compounding the economic and financial costs.”

In an interview with The Hindu, then (2012) chairman of Indian Oil Corporation RS Butola explained, “It [under-recovery] is a real loss of revenue. Under-recovery is the difference between the procurement price of products and their selling prices. While the procurement prices, which are import-parity based, change in line with international prices, the selling prices of sensitive products are controlled by the government. The difference between the two gives rise to under-recoveries.”

Three years ago Moneycontrol explained, “In the aftermath of the recession, oil manufacturing companies (OMCs) were facing large under-recoveries. This presented the government with the dilemma of ensuring the financial stability of OMCs, many of which are government-owned while taking into account the political repercussions of allowing fuel prices to rise. Oil bonds were chosen as the vehicle to dampen the pressure on OMCs while keeping prices in check.”

WHAT ARE OIL BONDS?

Oil Bonds, like all bonds, are essentially a form of a loan. Investopedia explains, “A bond is a fixed income instrument that represents a loan made by an investor to a borrower (typically corporate or governmental). Governments (at all levels) and corporations commonly use bonds in order to borrow money.” UPA issued them in order to meet the above-mentioned under-recoveries. Due to the low risk of bonds, they can be sold in the market. In July, it was reported that two OMCs who were issued these bonds sold them.

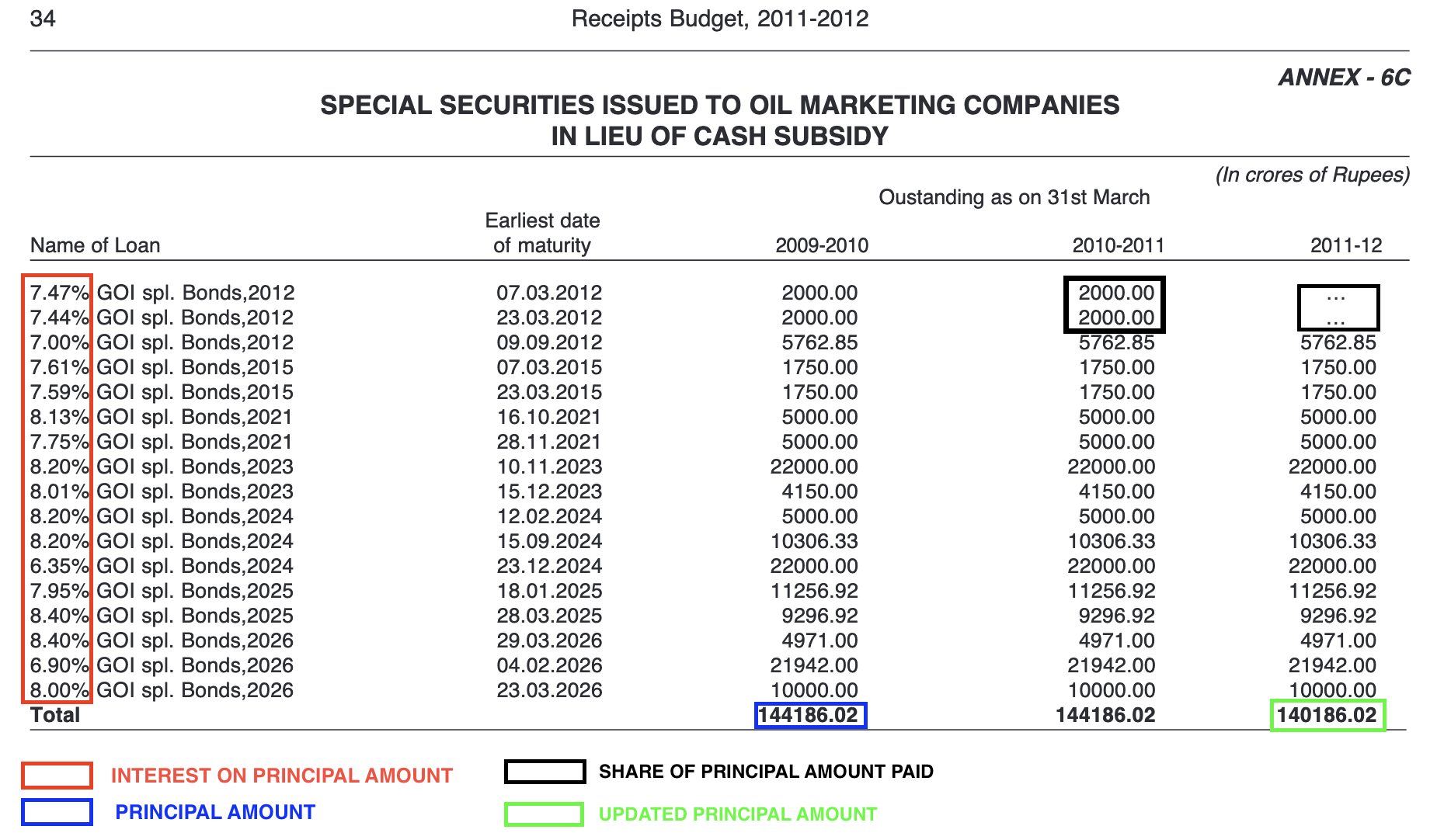

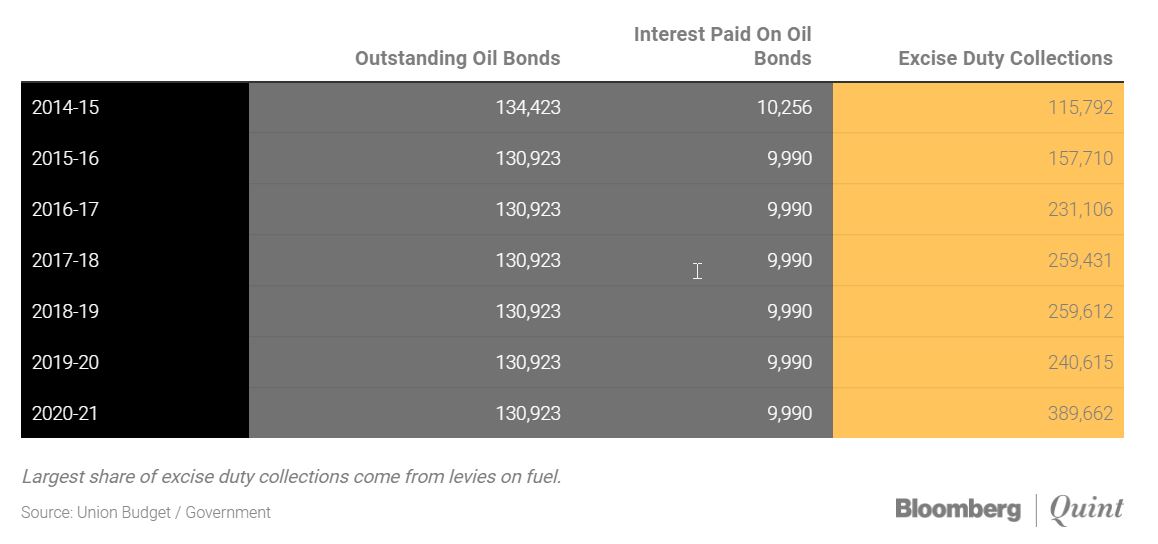

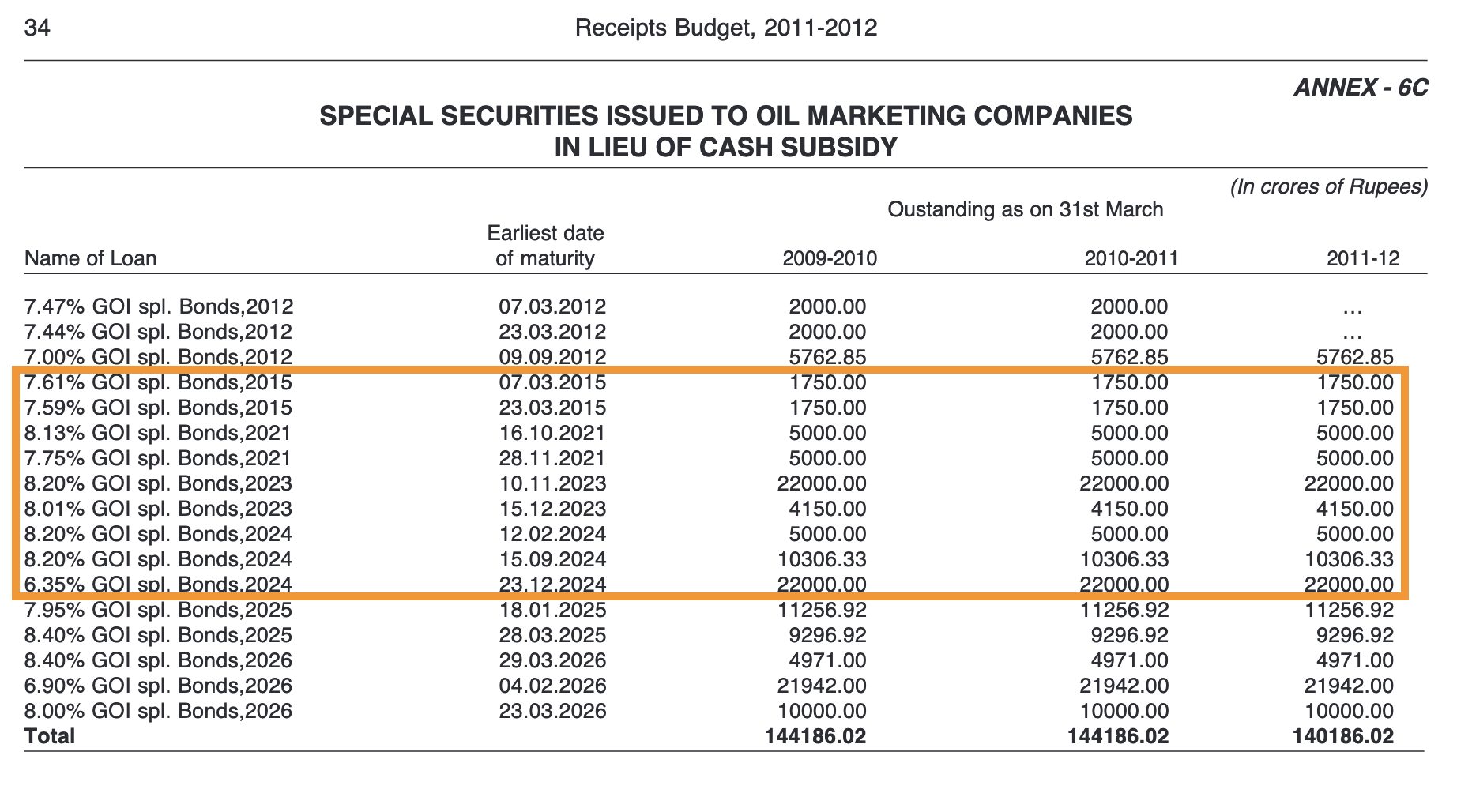

Ever since the 2011-12 budget, oil bonds have been featured distinctly in a dedicated section under the Receipts Budget section. As per the said budget, the amount of ₹1.44 lakh crores was to be paid in instalment over a period of 14 years along with interest. The maturity period of each instalment was pre-determined.

Bloomberg Quint (BQ) calculated the interest amount and it turns out that the BJP government has paid approximately ₹10,000 crores as interest on oil bonds each year from 2014 to 2021: that’s roughly ₹70,000 crores. The readers should note that the interest amount has been rounded off by BQ.

In addition to the annual interest on the principal amount of oil bonds (1.44 lakh crores), the BJP government has paid ₹3,500 (₹1,750 x 2) crores of the principal amount in 2015. By 2024, the BJP government would have paid ₹73,456.33 (orange highlight) crores of the principal amount including ₹10,000 (₹5,000 x 2) crores later in 2021.

ARE FUEL PRICES HIGH BECAUSE OF OIL BONDS?

However, Union Finance Minister Nirmala Sitharaman’s claim, “If I didn’t have the burden of oil bonds, I would have been in a position to reduce excise duty on fuel,” doesn’t hold merit because earnings (highlighted in red) from the petroleum sector to the central government is significantly higher than interest on oil bonds and total principal due until 2024.

In the 2020-21 financial year, the Central government earned over ₹4.5 lakh crores from the petroleum sector. That’s over 3 times [1.44*3=4.32] the total cost of oil bonds issued by UPA. Similarly, in the same year, the annual interest on oil bonds constitutes about 2.2% of the revenue from petroleum in 2020-21. [₹9,990/₹4,53,812*100].

Several media outlets, journalists, and social media users, including former finance minister P. Chidambaram, have called out the misleading claim.

The FM’s statement that servicing oil bonds stands in the way of giving relief on petrol and diesel prices is astonishing.

At best the statement is incredible ignorance; at the worst it is motivated malignity.

— P. Chidambaram (@PChidambaram_IN) August 17, 2021